Challenges under Place of supply of Goods

Challenges under POS for Goods

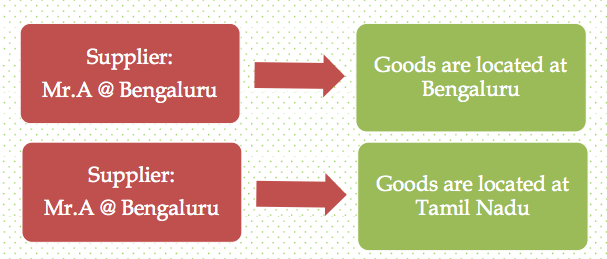

S.10(1)(a) of IGST Act: where the supply involves movement of goods, whether by the supplier or the recipient or by any other person, the place of supply of such goods shall be the location of the goods at the time at which the movement of goods terminates ―for delivery‖ to the recipient Challenges:

- Recipient picks up the material at door step of Supplier and destination of such goods is not known to the Supplier [B2C]2) Location of Recipient is known, however no clarity exists even to recipient for point of Delivery or change of destination in transit3) Recipient from different State picks up the goods from Supplier on his own account. Recipient may take back goods to his state or rest its movement in the state of the Supplier

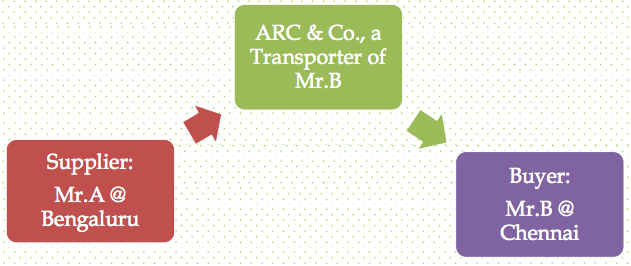

S.10(1)(b) of IGST Act:

where the goods are delivered by the supplier to a recipient or any other person on the direction of a third person, whether acting as an agent or otherwise, before or during movement of goods, either by way of transfer of documents of title to the goods or otherwise, it shall be deemed that the said third person has received the goods and the place of supply of such goods shall be the principal place of business of such person; Challenges:

- Head Office located in State 1 gives an Instruction to the Supplier for making the Supply of Goods to its Branch located in State 22) Goods are picked up by Recipient registered in TN from a Supplier located in KAR, which are meant for delivery to a Job-worker in Kerala3) Supplier in State1 removes the goods for delivery to the recipient in State2 as per the instruction of third person situated in State3. In transit, third person instructs the Supplier to give the delivery in State4

S.10(1)(c) of IGST Act:

where the supply does not involve movement of goods, whether by the supplier or the recipient, the place of supply shall be the location of such goods at the time of the delivery to the recipient Challenges: Head Office is located in State1, Branch is located in State2. Goods intended for Supply are located in State2. Branch enters into a contract on behalf of Head Office for Supply of Goods to a Recipient in State 3.

S.10(1)(d) of IGST Act:

where the goods are assembled or installed at site, the place of supply shall be the place of such installation or assembly; Challenges:

- Supplier in State1 make a supply to Recipient in State2 as per an Individual contract. Post receipt of goods, Recipient raise a request for Assembly cum Installation in State2 by virtue of another new contract.2) Supplier [B1] in State1 along with its Branch [B2]in State2 pools the goods to a Recipient in State3 for the activity of Supply cum Assembly/ Installation in State33) Branch 1 of the Supplier in State1 makes the supply of goods to Recipient in State2 and requests the Branch3 in State3, towards Assembly cum Installation at State2

S.10(1)(e) of IGST Act:

where the goods are supplied on board a conveyance, including a vessel, an aircraft, a train or a motor vehicle, the place of supply shall be the location at which such goods are taken on board. Challenges: Supplier Mr.X loads the food stuff on a Train which shuttles between Bengaluru to Chennai, to-fro. Food taken on Board shall be distributed at the beginning of the journey. Food loaded at Bengaluru for both the to & fro trips.

Challenges under POS for Goods – Import/Export

S.11 of IGST Act:

(a) imported into India shall be the location of the importer;(b) exported from India shall be the location outside India

Challenges:

- Head office of M/s.ABC Ltd., is in Mumbai. Goods are consigned from Germany to Recipient in Mumbai. Due to unfavourable climatic conditions, Head Office instructs the Branch in Chennai to take the delivery of goods2) M/s. PPC Ltd., supplier located in Kerala, supplies goods to Mr.A, an Exporter of goods Located in Chennai. Identification of POS when, Mr.A exports part consignment of goods to Germany and part consignment to Delhi

Recommended Articles

GST QuizGST RulesReturns Under GSTGST RegistrationGST RateGST FormsHSN Code ListGST LoginGST SoftwareGST Suvidha ProviderState GST Act