a) He is in possession of Tax Invoice/ Dr. Note/Prescribed Tax paying document.b) He has actually received the goods and/ or Services.c) Tax charged in the invoice has actually been paid.d) He has furnished required return under the GST Law. Before going to the Matching concept firstly we need to understand the GST returns:

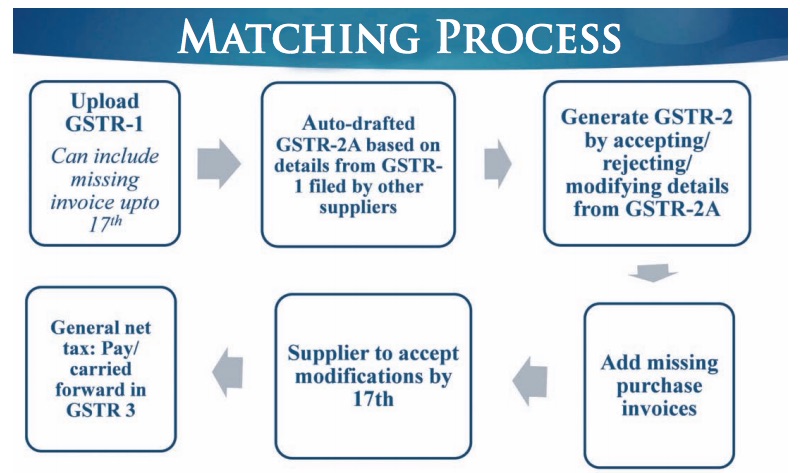

1. GSTR-1 (Details of Outward Supplies)

Section 37of CGST Act Read with Return Rule 1 casts an obligation on every registered person to furnish:

Detail of outward supplies of goods or services or both .During a tax period;Electronically through the common GST portal of GSTN.On or before the 10th day of the month succeeding the said tax periodIn Form GSTR 1

An Input Service distributor, a non-resident taxable person, a person availing composition scheme as provided u/s 10 or a person liable to deduct tax at source are not required to file return under this section Outward supplies details shall include details relating to the followings:

Taxable outward supplies comprising interstate supplies, intrastate supplies, Zero-rated supplies,Debit notes, credit notes and supplementary invoices issued during the said tax periodNil rated, exempted and Non GST Outward suppliesExportsAdvances received and Tax Invoices issued for the sameSupplies made though E-Commerce operator

The details of outward supplies so furnished by the supplier shall be made available electronically to the concerned registered person in Part A of Form GSTR 2A after due date of filling Form GSTR 1.

2. GSTR 2 (Details of Inward Supply)

In terms of Section 38 every registered person shall verify, validate, modify or delete the details of outward supplies by the supplier as communicated to him and may include the details of inward supplies and credit or debit notes that have not been declared by the supplier in GSTR 1 and shall furnish

Details of inward supplies of goods or services or bothMade during a tax periodElectronically through a common portal of GSTNOn or before the 15th day of the month succeeding the said tax periodIn Form GSTR-2

An Input Service distributor, a non-resident taxable person, a person availingcomposition scheme as provided u/s 10 or a person who is liable to deduct tax at source are not required to file return under this section. Inward supplies details GSTR-2 shall include details relating to the followings:

Inward supply on which tax is payable under reverse charge basisInter-state suppliesDebit notes, credit notes and supplementary invoices issued during the said tax period.Inward supplies on which IGST is payable under section 3 of Customs i.e. import

3. GSTR 3 (Monthly GST Returns)

Every registered taxable person, other than input service distributor or a non resident taxable person or a person availing composition scheme or person liable to deduct or collect tax, shall for every calendar month furnish a return in Form GSTR 3 Electronically of inward and outward supply, Input Tax Credit availed, Tax payable, tax paid and such other particulars, on or before 20th of the succeeding month. All the claims of ITC as self-assessed shall be provisionally accepted as per section 41 and shall be credited in electronic credit ledger of the registered person. However if the supplier has not made the payment of tax payable or not filed the monthly return, the ITC so claimed on provision basis will be denied later in the hands of the recipient of the goods or services or both.

Matching Concept of ITC under GST

Once the supplier and recipient has filed outward and inward supplies details as per Form GSTR1 and GSTR 2 respectively and the monthly return on Form GSTR 3 , the details of inward supply furnished by the recipient shall be matched with the corresponding details of outward supply furnished by the supplier in his return for the same or earlier tax period. In the process of such matching, the details of inward supplies which matches with the details of outward supplies shall be finally accepted and shall be accordingly communicated to the recipient. The mismatch can be of the following nature

a) Input tax credit availed by the recipient is more than the tax declared by the supplierb) Input tax credit availed by the recipient but outward supply is not declared by the supplierc) Duplication of claim of Input Tax Credit by the recipient

In case of mismatch in the nature of clause (a) or (b), the discrepancy shall be communicated to both the supplier and recipient with an option to rectify the discrepancy in the return for the month in which the discrepancy is communicated. As far as mismatch on account of duplication of claim of input tax credit is concerned, the discrepancy shall be communicated only to the recipient and the excess amount shall be added to the output tax liability of the recipient of the same month in which discrepancy is communicated. With regard to mismatch under clause (a) and (b) above, once the communication is made, the supplier or recipient shall accordingly rectify the discrepancy in the return for the month in which the discrepancy is communicated. However if the discrepancy is ultimately not rectified by the supplier or recipient, the tax discrepancy shall be added to the output tax liability as under

a. If supplier does not rectifies the discrepancy then the excess input tax credit so availed by the recipient shall be added to the output tax liability of the purchasing dealer i.e. recipient in the month succeeding the month in which the discrepancy is communicated along with due interest from the date of availing of credit till the corresponding additions made in his return.b. If the supplier later on declares the details of the Invoice and/or debit note in his valid return then the recipient shall be eligible to reduce his output tax liability which was added earlier in his return. Any interest paid earlier shall also be refunded to the purchasing dealer.

Matching of Credit Note

As stated here in above, every supplier has to furnish the details of invoices, credit notes or debit notes, etc. in its outward supplies details in Form GSTR 1. A credit note is generally issued for reduction in taxable value or tax charged in tax invoice or for return of goods or for deficient supply. Since the supplier has initially paid the taxes on the basis of tax invoice and recipient has also availed the credit on the basis of such tax invoice and now credit note reduces the output tax liability in the hands of supplier, the same is allowed only if the recipient has also reduces his claim of input tax Credit. Section 43 provides for matching of credit note issued by supplier with simultaneous reduction in claim of input tax credit by the recipient and for duplication of claim of credit note by supplier resulting in reduction in output tax liability. In the process of such matching, the claim of reduction in output tax liability by the supplier that matches with the corresponding reduction in claim for input tax credit by recipient shall be finally accepted and shall be accordingly communicated to the supplier. The mismatch can be of the following nature

d) Reduction in output tax liability by the supplier is more than the corresponding reduction in claim of input tax credit tax by the recipiente) Credit note is not declared by the recipientf) Duplication of claim for reduction in output tax liability by the supplier

In case of mismatch in the nature of clause (a) or (b), the discrepancy shall be communicated to both the supplier and recipient with an option to rectify the discrepancy in the return for the month in which the discrepancy is communicated. As far as mismatch on account of duplication of claim for reduction in output tax liability is concerned, the discrepancy shall be communicated only to the supplier and the excess amount shall be added to the output tax liability of the supplier of the same month in which discrepancy is communicated. With regard to mismatch under clause (a) and (b) above, once the communication is made, the supplier or recipient shall accordingly rectify the discrepancy in the return for the month in which the discrepancy is communicated. However if the discrepancy is ultimately not rectified by the supplier or recipient, the tax discrepancy shall be added to the output tax liability as under

a. If recipient does not rectifies the discrepancy then the same shall be added to the output tax liability of the supplier in the month succeeding the month in which the discrepancy is communicated along with due interest from the date of claim for reduction in output tax liability till the corresponding additions made in his return. b. If the recipient later on declares the details of the credit notes in his valid return then the supplier shall be eligible to reduce his output tax liability which was added earlier in his return. Any interest paid earlier shall also be refunded to the purchasing dealer.

Here it would be relevant to note that, no such rectification of invoices/reclaim of input tax credit shall be allowed after due date for filing of return for the month of September of the following year or date of filing of Annual Return, whichever is earlier. For example, if the invoice pertains to Financial year 2016-17, then in that case it should be rectified before filing the return of September 2017 i.e 20th October 2017 or date of filing of annual return for F.Y. 2016-17 whichever is earlier, It is important to note that in case such period lapses, no such rectification is allowed and input tax credit related to them will be lost. This mechanism of matching seems to be highly automated and thus all the returns of selling dealer as well as purchasing dealer will be linked with each other, so that any change on one side will be correspondingly reflected on the other side. Therefore, both the seller as well as purchaser is required to be very careful in filing the returns and in uploading sale / purchase details. Even a slight mismatch in the details will lead to unnecessary demands and may also lead to litigation for recovery of tax. Recommended Articles

When will GST be applicableGST ScopeFiling of GST ReturnsReturns Under GSTGST RegistrationGST RatesGST FormsSystem Requirements for Using the GST PortalGST Registration FormatsHSN Code ListGST LoginGST Registration last dateGST Due Dates