ISD under GST, Input Service Distributor

ISD is an office of a person (having same PAN) which receives tax invoices towards receipt of input and issues tax invoice thus acts as input service distributor for the person. An ISD is required to obtain registration as a deemed supplier of services.

- Every Input Service Distributor shall, after adding, correcting or deleting the details contained in FORM GSTR-6A, furnish electronically a return in FORM GSTR-6, containing the details of tax invoices on which credit has been received and those issued.

- The distribution of credit would be done subject to the following conditions;

a) Credit should be distributed through tax invoice or document as prescribedb) Amount of credit distributed should not exceed available credit.c) Credit only to such suppliers whom such services are attributable.d) Credit on propionate to respective turnover during the preceding financial year basis if more than one attributable suppliers.

- One company can have multiple register ISD offices like marketing division, security division etc.

- ISD may distribute the GST as under;

Conditions for distribution of input tax credit by an ISD

The amount of credit distributed shall not exceed the amount of credit available for distribution.Invoice must state that ‘it is issued only for distribution of input tax credit’, should be issued by the distributor to the recipient of credit. ITC (input tax credit) available for distribution in the same month, and the details of the same shall be furnished in Form GSTR -6 within 13th of the next month.The input tax credit should be distributed only to that branch which has consumed the input servicesThe credit of tax paid on input services, availed by more than one recipient of credit or all, should be distributed only amongst such recipients or all recipients.

Method of input tax distribution The distribution shall be on pro rata basis based on the turnover for the previous year of such recipients. In the absence of turnover in previous financial year, the turnover of the last quarter of the month in which ITC is distributed, will be considered. If ‘Debit note/ Credit Note’ raised by a supplier to the ISD shall be apportioned to each recipient in the same ratio in which the input tax credit contained in the original invoice was distributed. The distribution should be on the basis of method as above. In the ISD credit note same as contain details as per point No 1 . The reduction amount so apportioned should be:

Reduced from the amount to be distributed in the month in which the credit note is included in the return in FORM GSTR – 6 andAdded to the output tax liability of the recipient, in case the amount so apportioned is negative

Input Service Distributor under GST Regime, ISD Under GST Regime 2017

Input Service Distributor (ISD) is defined in Section 2(54) of the Model GST Law, which is reproduced below: “Input Service Distributor” means an office of the supplier of goods and/ or services which receives tax invoices issued under section 28 towards receipt of input services and issues a prescribed document for the purposes of distributing the credit of CGST (SGST in State Acts) and / or IGST paid on the said services to a supplier of taxable goods and / or services having same PAN as that of the office referred to above; It is to be noted that under GST Regime as well, a separate registration is to be taken as Input Service Distributor (ISD) even though the office may be registered as taxable person. From the definition it can be observed that there must be inward supply of services along with tax invoices issued under section 28 to the Input Service Distributor and he in turn can distribute the credit to his other units who must be a supplier of taxable goods and/or services having the same Permanent Account Number (PAN) so that they can avail/utilize the credit against their output tax liability. These following points are of utmost importance:

The tax invoice should be received by ISD toward inward supply of services. Goods have not been covered under the provisions of ISD.Prescribed document is to be issued.The unit/branch receiving the credit must be a supplier of taxable goods and/or services. If he is supplying exempted goods alone he is not eligible to receive the credit from ISD.The unit/branch should be registered under the same PAN as that of ISD.

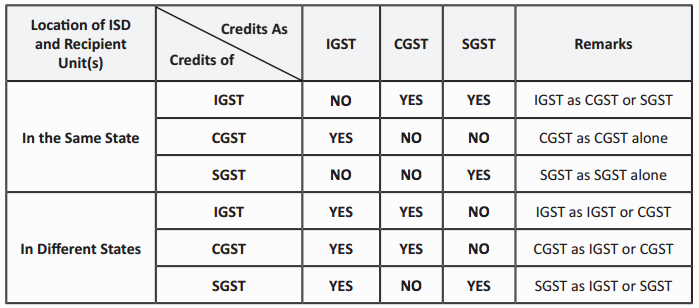

Section 21 of the Model GST Law prescribes the manner in which credits of CGST (SGST in State Acts) and/or IGST can be distributed to other units/branches. In this regard distinction is made on the manner of distribution of credit when the Distributor and Recipient are in Different States and when they are in same states. The relevant manner of distributing the credit subject to certain general conditions is laid down below:

Where the Distributor and Recipient are in DIFFIRENT States

The ISD may distribute credit of CGST as CGST or IGSTThe ISD may distribute credit of IGST as IGST or CGSTThe ISD may distribute credit of SGST as SGST or IGST

Where the Distributor and Recipient are in SAME States

The ISD may distribute credit of CGST as CGST aloneThe ISD may distribute credit of IGST as CGST or SGSTThe ISD may distribute credit of SGST as SGST alone

The above provisions can be summarized in the table below: It may be noted that where credit can be distributed as either of the two alternatives, the one which is most beneficial should be opted for. For example, assuming distributor and the recipient are in same state, where one unit/business vertical has a huge CGST liability, the IGST credit should be distributed by the ISD as CGST (and not SGST) to that particular unit/vertical, so that it will be able to set off its liability with the credit to the maximum extent possible and less amount may be paid via cash. Accordingly, if there is another unit/vertical with more SGST liability and SGST input credit of that unit is insufficient to cover the same, the IGST may be distributed, to that particular unit, as SGST. The Law has provided certain overall conditions subject to which the distribution as referred above can be effected. These provisions are highlighted below:

the credit of tax paid on input services attributable to a recipient of service (i.e. one particular unit among many) shall be distributed only to that recipient (unit). In other words, we are allocating the credit and not distributing the same. Wherever a direct nexus is established between the value of input services and the unit utilizing those services, the input credit on such services is to be distribution/allocated to that particular unit.the credit of tax paid on input services attributable to more than one recipient of credit shall be distributed only amongst such recipient(s) to whom the input service is attributable and such distribution shall be pro rata on the basis of turnover in a State of such recipient, during the preceding financial year if the recipients have turnover during that year or, if some or all recipients do not have turnover during the preceding financial year, during the last quarter for which details of such turnover of all the recipients are available, previous to the month during which credit is to be distributed

to the aggregate of the turnover of all such recipients to whom such input service is attributable and which are operational in the current year, during the said relevant period. The word turnover means aggregate value of turnover defined under sub-section (6) of Section 2.

The credit attributable to all recipients shall be distributed amongst such recipients on pro rata basis of turnover in State.The amount of credit distributed shall not exceed amount of credit available for distribution.The prescribed document shall be issued to each recipient of credit and shall contain such details as may be prescribed.

Further, Section 22 provides that where ISD distributes credit in excess of what is allowed and provided under section 21, the excess may be recovered from the recipient(s) along with interest and the provisions of section 66 and 67, as the case may be, shall apply mutatis mutandis for effecting such recovery. Unlike the existing law, the GST Model Law differs in its view when it comes to the recipient to whom the input credit can be distributed by the ISD. Under the existing laws, the credit was not restricted to any particular unit or manufacturer or service provider and the credit of services utilized by one unit was allowed to be distributed to another unit. The CESTAT, Bangalore in the case of Ecof Industries Pvt. Ltd. v. CCE, Bangalore 2009 (10) TMI 171 adopted a holistic view and held that the availability of credit is related to manufacturer of goods or provider of output services as a whole and is not restricted to any particular unit or manufacturer or service provider. On a further appeal by the revenue, the Karnataka High Court later in 2011 concurred with the view of CESTAT, Bangalore, and the appeal was disposed in favour of the assesse. Not upholding similar position under the GST Regime, will definitely cause undue hardship to taxpayers. The relief might be available in the due course in the form of similar judicial pronouncement(s) but of that we are unsure as of yet. We just have to wait until GST rolls out and sheds more light on various unclear issues. Recommended Articles –

Karnataka GST ActGST Registration ProcedureState GST ActGST DownloadsReturns Under GSTGST RegistrationGST RatesGST FormsHSN Code ListGST LoginGST Registration last dateGST Due DatesGST Rules