Concept of Revenue Neutral Rate under GST

Revenue Neutral Rate is an important concept in GST regime, as per Law Lexicon Dictionary by P. Ramanath Aiyar “Changes in the tax law which result in the same amount of overall total revenue”. There will no increase or decrease in the revenue of government after giving or providing any setoff/deductions/rebate to the tax payers. Suppose if government has given some tax rebate to the individuals by increasing tax rate on corporations. The tax rebate on individuals will be compensated against the tax on corporations. The net collection for the government will be same as before giving rebate to the individuals. Now in the context of GST, Revenue Neutral Rate is the rate at which tax revenue of the Central Government and State Government will remain the same under proposed GST as is under the present Indirect Tax structure in India. The RNR is treated as a factor which will keep the revenue of governments under GST regime same as in Indirect Tax Structure applicable in India. Example: let us consider an example suppose in state A people’s expenditure the whole year is Rs. 2,00,000 Crore, now to collect Rs. 20,000 Crores as taxes the Government levied tax @10%. When due to some compulsions the government provides exemption to the tune of Rs. 40,000 Cores on expenditure to the people. Then to collect Rs. 20, 0000 Crores, the government will charge @16% instead of @10% earlier. Now in this case rate @16% will be Revenue Neutral Rate. The Kelkar Task Force Report has suggested the RNR rate will be @20%, which will be divided between Centre and State at the rate of @12% and @8% respectively. But this rate is very high as compared to other countries where GST is applicable. These countries have applied GST on all types of transactions without giving exemptions. They have expended the base of GST keeping rate low @3% in Singapore and @10% in New Zealand. Now in India it is difficult to decide RNR due to various exemptions and threshold limit provided in different states by state as well as central governments.

Factors Influencing RNR:

- Threshold Limit: Is a quantum of turnover below which firms, manufactures, traders, dealers or service providers got the privilege not to register/pay tax under respective statue. We can say that threshold limit is that quantum of turnover below which any dealer, manufacture, trader or service provider in not bound to register with statutory authorities and pay taxes. Central Government has provided threshold limit in case of Central Excise up to Rs.1.50 Crore and Rs. 10.00 Lakhs in case of Service Tax. The State Governments also has provided threshold limits in VAT due to political pressure or welfare regime in the state. As we know if the threshold limit is lower in a tax regime, then to achieve the same amount of tax, one has to increase tax rate on the taxable quantum. The low threshold limit enables government to lower rate of tax. But when we are going to increase tax base, the administrative cost will increase. So while deciding RNR it is important to consider all factors, which will influence the rate of tax. C-Efficiency Ratio: The International Monitory Fund (IMF) devised C-Efficiency ratio to monitor RNR. Note: any deviation from a 100% C-Efficiency indicates deviation from single tax rate on all consumptions. If government gives exemptions or make any consumption as zero rated then the C-Efficiency ration will be less than 100% or if government added more items to be taxed then the rate will be above of 100%. Example: Lets us consider an example , assume Private Final Consumption Expenditure of any state for one year is Rs. 10,00,000 and the rate of GST is @20%, then according to C-Efficiency Formula; Note: The above example shows that if there will be some exemption or zero rated expenditure then the C-Efficiency will be less than 100% and affects the rate of GST. Thus the exemptions limit effects RNR rate, if threshold limit will be lower than RNR will be lower and if threshold limit is higher than RNR will also be higher. 2 ZERO RATED GOODS AND SERVICES THAN EXEMPTED GOODS AND SERVICES: Exemption as the term denotes is used to define a product or service which is exempted under a regime of tax and service provider or seller of the product will not charge any tax on the same. As we know the transportation services related to transport of food grains has been exempted from service tax. The service provider, the transport agency does not charge Service Tax from the service recipient as well as not allowed to take CENVAT Credit on input services used in providing output Service. Lest us consider an example Mr. A, a transport service provider is providing services to Mr. B in tax free economy. The cost of service for Mr. A is Rs. 90/- and his margin is Rs. 10/- , now the service provided by Mr. A to Mr. B is exempted and Mr. A con not claim CENVAT credit of the input service used by him in providing output service to Mr. B , suppose it is Rs. 9/-. Now in tax free regime Mr. A will add Rs. 9/- in the cost of providing services to Mr. B and the cost will be Rs. 99/- instead of Rs. 90/-. Now he will claim Rs. 108.90/- from Mr. B adding his profit margin. Now this cost 108.90/- will bear by Mr. B without getting any setoff under CENVAT Rules and ultimately the tax burden will pass to the consumers. Now in tax regime Mr. A will charge Rs. 110/-(Rs. 100 + 10 profit margin) and he is eligible to claim Rs. 9/- as setoff as CENVAT Credit. Now Mr. B is bearing burden of Rs. 9.90/- as taxes paid to Mr., if Mr. B. is not eligible to CENVAT Credit then the cost of production will increase and Mr. B will charge the same from consumers. Now in Zero rated services , if Mr. A is rendering Zero Rated services then he will not charge any tax on his services provided to Mr. B, now in this case, whatever he has paid as taxes on input services i.e. Rs. 9/-, will be refunded to him by the Revenue Department. Now in this case the real benefit will pass to the final consumers. The Exemptions and Zero Rated will increase the RNR rate and effects Standard Rate of GST.

3. Zero Rated Exports;

means when the Goods and Services are exported out of country and no GST would be charged on them. Now in this case if the GST is charged on input Goods and Services, same would be refunded to the exporter. This is for betterment of exports and competitiveness in the World Market. Many countries provide various types of exemptions to increase their export and to compete in the export market. Since in GST the Goods and Services would be taxed on the basis of point of consumption not on the basis of Origin. Now this loss of revenue due to Zero Rated Exports would nevertheless be compensated by imposing additional burden of GST on other items of Goods and Services. 4. Exemption and Lower Rate of tax for certain items such as Food, Healthcare Etc.: The Government Should impose GST on all Goods and Services for better tax management but due to welfare and social services it has exempted or taxed with lower rate of some Goods such as Food grains and Services such as Health Care, Education as these are important for the people living below poverty line. The Organization for Economic C-operation and Development (OECD) Publication 2004 sets out “Standard Exemptions” in GST system for OECD countries. These “ Standard Exemptions” includes Hospital and Medical care, Transport of Sick and injured person, Human Blood, Tissue Organs, Dental care, Postal Services, Education, Non Commercial Activities of Non Profit making organizations, Cultural Services, Radio and Television broadcasting services etc. Some countries adopted “Standard Exemptions” as provided by OECD and some has been departed such as New Zealand it has applied tax on all Goods and Services listed above. In India taxing food items will cost live of poor and as a welfare state, it is duty of the government to take care of people below poverty line. Now in these cases the RNR rate will increase.

5. Exemption Mechanism for Special Industrial Area:

The Government is providing various tax exemptions to the industries established in less develop areas of North Eastern Ares, Jammu and Kashmir, Himanchal Pradesh, etc., as we know these exemptions are not working properly and gave chance of corruption and erosion of taxes. These exemptions are generally given for attracting investment and development of areas but are not working properly. These would have negative impact on GST and may increase RNR rates.

6. Compounding Scheme under GST:

There are various compounding and composition schemes in present Indirect tax regime. These are issued to help small traders, manufacturers and service providers. Under this scheme the government has set some threshold limit under which traders,manufactures and dealers may opt to pay specified some of duty or pay at specified rate as prescribed without taking relevant credit on taxes paid on input goods and services. On other hand he has to pay full tax levied on goods and services after taking full tax credit of taxes paid on input goods and services. 7. Abatements; it is a partial exemption from payment of total taxes levied. As we know government has provided abetments related to various services through Notification No. 26/2012 dated 20/06/2012. If abetments would be provided in GST also as provided in recent scheme, then this would impact negatively and RNR would increase to compensate this revenue loss. Other various incentives and exemption schemes of the government would impact GST and hence it is necessary to think twice about these schemes and incentives before implementing GST regime.

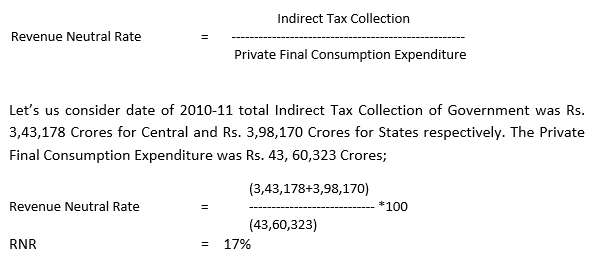

Calculation of Revenue Neutral Rate

Note: from above details we can analyze that the RNR will go up is we provide incentives, rebates, abetments, exemptions or compounding and other various incentives. We hope that our Central Government would act fast to implement the GST in India to give much needed gift to the business fraternity.

GST RateGST Registration StatusGST LoginHow to Register and Update DSCGST RegistrationGST FormsHSN Code ListITC under GSTGST Due DatesTax Payment in GSTGST RefundPlace of Supply under GSTReturns Under GSTGSTR 1 Return Checklist